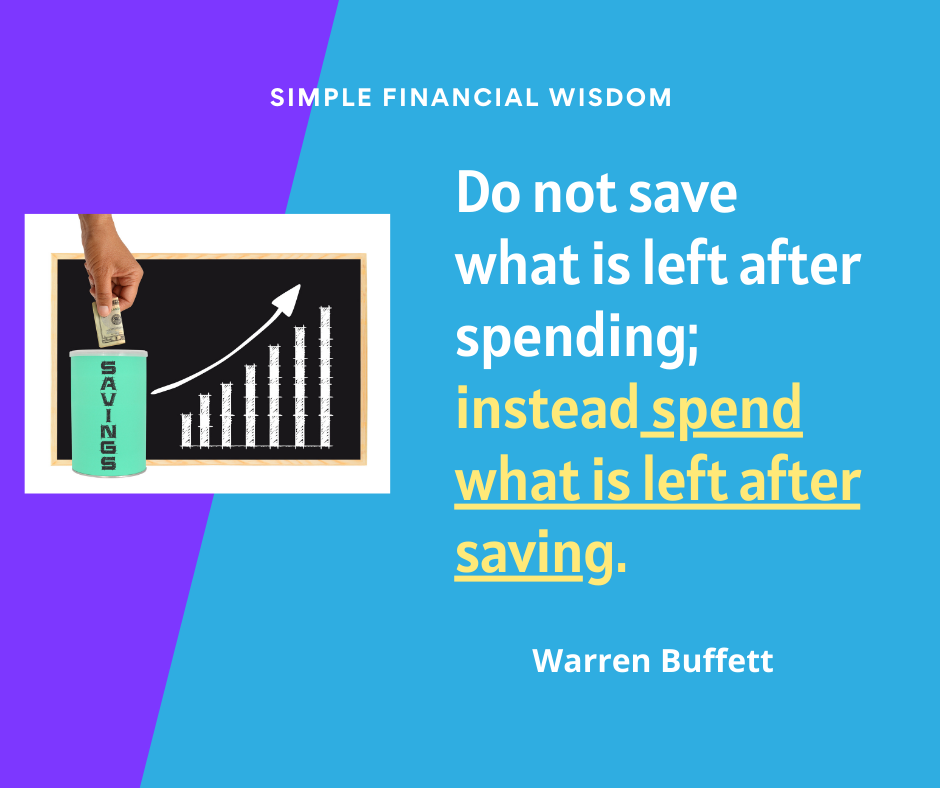

Financial Wisdom from Warren Buffet

Perhaps you have the best intentions to save money, but still have zero savings. Nada. Nilch. None.

Perhaps you have the best intentions to save money, but still have zero savings. Nada. Nilch. None.

If you truly want to learn to save money but have tried and failed (spending it on fast food and Amazon, you say?), then what might be lacking is a place to start and a path to follow.

What?

You need to establish a habit of saving money.

To establish that habit, you need to have a set of rules and a starting point. The beginning rules should be very simple and very easy.

For this money saving habit, you will start with a tiny amount and keep repeating. And repeating. Until you reach a point that it feels disturbing to skip the habit, even once. When you reach that point, the habit has become locked in a neuron path in your brain.

You can now start increasing the amount that you save – in small increments that get larger over time. One day in the not so distant future, you will be surprised at how much and how easily you put money into your savings.

Here is an example of how to start saving money – perhaps it was the easiest example until COVID created a coin shortage!

In this example, you set a rule: Save one coin every week by Friday at midnight. That’s it. Just one coin, even a penny. Starting right now.

You find a jar (or a box or a container) and set it on your dresser. Deposit your first coin and your habit has begun.

Do not go out a buy a fancy piggy bank or jug for your coins. Start with what you have. When you have reached a milestone … say 12 weeks of faithful saving, then you can get yourself something better if you still want it. But don’t reward yourself by buying a fancy savings container at the start of the new habit. Make yourself earn the reward. If you reward yourself before you start, you fool yourself into thinking you have already accomplished your goal and your mind begins to lose interest.

After a couple of weeks, if you want to add in miscellaneous pocket change or even a dollar bill or two, go ahead. But don’t change the rule. One coin. Once a week. That is all it takes for you to have a successful week. After a few weeks, step up your game. Increase the required number of coins or make it two days a week. Yet stay within a limit that you know you can reach. Don’t try to jump from saving a few coins once a week to saving a $20 bill once a week. It’s better to go from a coin, to a few coins, to a $1 bill, to a $5 bill over time.

Create reminders and make absolutely no excuses. If you wake up and remember that you forgot to save your coin, then get out of bed right away and find a coin to deposit in your savings bank! Self discipline means you follow through on your commitments even if it is inconvenient, even if you are tired or had a bad day, and especially when there is a voice in your mind insisting that it doesn’t really matter if you skip this one time. It matters.

You are doing two things right now. First, establishing a habit – repeating it until it is naturally and permanently a part of your routine. Second, you are changing your self image from an image of one who “can’t save money” to one of “I save money on a set basis without fail.”

Once you are hard wired to save money, you will be surprised at the ideas and opportunities that begin to appear that will help you to begin to grow your savings.

Now, our example was saving coins in a jar. No coins? Perhaps you can put $1.00 in your savings account every time you get a paycheck. Or every Tuesday you can drink water at lunch instead of a soft drink and then transfer the price of the soft drink into your savings account. (Hint, make it really easy and calculate the soft drink cost once and continue to use the same figure week after week. )

You make the rules. Make them easy, with a set time and place to perform, and at an initially very low set amount.

Look at you. Now you are a person who makes a habit of saving money. You are awesome!

Share your rules and your progress in the comments!

New Year’s Day brings a celebration of new beginnings, but it also rings in a new tax season. For many, the rush is on to file their income tax return at the earliest possible moment. Most likely this is due to the promise of a large tax refund.

New Year’s Day brings a celebration of new beginnings, but it also rings in a new tax season. For many, the rush is on to file their income tax return at the earliest possible moment. Most likely this is due to the promise of a large tax refund.

Yes, it is good to get your tax refund quickly so you can use it to pay down bills or add to your investments. But not if your haste causes you to file an incorrect tax return. This could be costly in the long run.

What kind of problems might be created with a tax return filed in a rush? Here are the most common issues:

In the rush to file, it is easy to forget that you worked a couple of weekends at a second job, earned some interest on an account that you closed last year, or that you sold a small amount of stocks a year ago. Many companies wait until the deadline (usually Jan 31st) to issue the respective W-2’s or 1099s. You might not receive the necessary tax forms until well after the 1st of February. For forms other than 1099-MISC and W-2’s the company may request an extension of time to file which would further delay your receipt of the forms.

Recent tax laws increased the standard deduction. However, if you have a large or high interest rate mortgage, large donations to charity, paid large medical bills, or paid a large amount of state and local taxes, you should check to see if you still might be able to itemize deductions. If you can, then slow down and carefully check your receipts and bank account registers for deductible expenses that you may have overlooked.

This is even more important for the small business owner with Schedule C (self-employment) income. Check your personal accounts for business expenses you paid that have not yet been posted to your books.

Even without itemizing, there are deductions that can be taken, such as education expenses, self-employed health insurance deductions, and deductions for contributions to traditional IRA accounts.

Unclaimed Credits

Unclaimed CreditsOverlooking credits can leave a lot of money on the table – thousands of dollars in some cases. Education credits, earned income tax credits, energy saving materials credits, credits for foreign taxes paid from stock and mutual funds, child tax credits, and child care expenses credits are some of the credits that can be overlooked when you are in a hurry to file.

The deduction for dependency exemptions has been eliminated, but the other benefits from claiming a dependent are still strongly in place. You could miss out on education credits, child tax credits, medical deductions, higher thresholds for health savings accounts, and higher earned income tax credits.

On the other hand, you could also claim a dependent that you are not qualified to claim. For example, say you trade your child’s exemption claim every other year with an ex-spouse. If in your haste you claim the exemption in the wrong year, yes you might get the extra benefits on the tax return. But it is highly likely that you will pay back that tax benefit either to the IRS (plus penalty and interest) or to the ex-spouse when they demand it, or worse, when they take you to court to correct it (add in your attorney fees to that one.)

Up until the due date of your Federal tax return, you can still consider a prior year deductible contribution to your traditional IRA account or your HSA account. However if you file the return early and then realize that you want to make the prior-year contribution, your only recourse is to make the timely contribution and then file an amended tax return to claim it.

If you are eligible to contribute to an HSA account and you have out-of- pocket medical bills coming up, it is financial insanity to not consider making a tax-deductible contribution to your HSA and then using that same money to pay the medical bill. Bingo. You just found a roundabout way to take a tax deduction for a medical expense even if you don’t have enough to itemize.

We are living in an age where the government seems to regularly pass tax laws just before or after Jan 1st. If you file too early, the tax forms might not even reflect the tax changes that were just made.

This could cause you to miss a deduction or credit (like the recently revived credit for adding insulation or energy-efficient windows to your home). It could also cause your tax return to go into a multi-week hold because the tax changes affected a small line item on your tax return and the IRS can’t process your return until their software is updated.

The IRS spends the last part of the year converting their software to the new tax year, updating for new legislation and regular yearly changes, as well as training their full time and temporary staff how to use the software, run the systems, and become knowledgeable about the new tax year’s laws and changes. Will the first week of filing be perfect? Nope. As hard as they have worked, there will be glitches, stalls, changes, quick revisions, and updates as the new tax year begins to roll. Early filers can easily get caught in these errors and delays of tax season start up. Waiting just a week or so while the new system is tested may make filing your tax return a much smoother process.

Of course it is. Just don’t file in a big, careless rush. Go back through your calendar to remind yourself of jobs, events, or expenses that might affect your return. Carefully check all parts of the tax return and double check that you have received all of your tax forms and taken advantage of all eligible credits and deductions.

About the author: Patti is a CPA and has a CPA firm in Elkhart IN. Her firm offers tax and accounting services to individuals and small businesses.

If you have an offbeat friend that likes odd things, you know better than to get them an ordinary or boring gift. Here are some ideas for inexpensive, odd gifts that are sure to be different:

If you want to honor their odd side and show you care deeply about their nutrition, give them an onion flavored seaweed brick.

2. Talking Toilet Paper Spindle

You can record your own message of bathroom encouragement. Now how thoughtful is that!?

The product description says “Hours of Mindless Entertainment” … what a perfect gift! It even includes batteries!

It is all-season! This will shield your pal from the sun AND from the rain. Sorry, not for high winds though. Manufacturer suggests it as a gift for your mailman. Hmmm.

5. Honor their oddness with an art print they can hang on the wall

“You have to be odd to be number one.” Well said, Dr. Seuss. Come to thing about it, he’s right.

They can make music for all to enjoy! Open the mouth to change the bass. It’s a portable synthesizer … bet your friend has always wanted one!

Well of course she’s been wanting a pair of these.

I suppose we should add a pair for the Cheetos freak:

This will only seem odd to the unenlightened. Actually a beautiful gift even if it is a little different. You can get one for me.

Why, this book is an absolute must for your cat-owning friends!

10. Venus Fly Trap

When you can’t think of anything else to give them. Claims to need no watering, feeding, or sunlight. You know which friend should have this.

There you have it. 10 ideas for that hard-to-buy-for person. Happy gifting!

Feel free to share your own ideas in the comments.

Mother Earth News has a fascinating article How to Save a Million Dollars With a Sustainable Lifestyle . The perspective is refreshing and right in line with The Fat Dollar philosophy.

Mother Earth News has a fascinating article How to Save a Million Dollars With a Sustainable Lifestyle . The perspective is refreshing and right in line with The Fat Dollar philosophy.

The short summary is that by switching to a lifestyle that depends less on gadgets, grid provided utilities, restaurants, resorts, and … (ouch!) cars, among other things, then you can save thousands upon thousand of dollars that will quickly accumulate to a million or more.

What kinds of changes? Here are a few:

– Avoid debt and save many thousands in interest

– Go from a two-or-more car family to a one-car family and save thousands on insurance, maintenance, and gasoline

– Find your own values to be passionate about and be less interested in the latest fashions, gadgets, or other status-type purchases

– Prepare food at home and save thousands on restaurant and pre-processed food while getting higher nutritional value

– Switch to active entertainment such as playing a musical instrument, talking with your spouse and neighbors, or practicing a craft and save money on passive entertainment like movies and spectator sports

– Buy a house only as large as you need, possibly after selling the one you are in and save thousands on interest, maintenance, furnishing, and decorating

I was fascinated at the magnitude of the claimed total savings in the article, but there were not really any calculations or proof to show how a typical family could really save a full million dollars with all these changes.

So I will offer some calculations for you:

For example, let’s say you made these changes:

– Cut back on food spending, saving $50.00 a week

– Sold one of your cars and saved $6000.00 a year in vehicle expenses

– Stopped going to the movies once a week and saved $30.00 a week

– Stopped buying status-type stuff and saved another $250.00 a month

– Sold your house and bought a smaller one, saving $6000.00 a year in

interest and another $3000.00 a year in maintenance and utilities

That would all add up to $22,160.00 in savings a year.

$22,160 is a remarkable number. A very remarkable number. That would make a huge difference in most family budgets.

However, assuming no interest on savings (which is not really hard to imagine today), it would take a little over 45 years of doing this each year to save a million dollars. That is not quick.

Even if you could assume 5% interest (and no income taxes) on your $22,160 yearly savings, it would be 25 years before you would accumulate a million dollars.

Of course, you could invest in the stock market. In that case, we will assume an 8% average rate of return on your $22,160 yearly savings. You would reach $1,000,000 in 20 years. Not bad, really. Not bad at all.

Alternatively, instead of investing every penny of your savings, you could choose to work fewer hours, or even change to jobs that pay less but bring much more enjoyment to your life. In that case, you would not be accumulating as much in savings, but your quality of life could dramatically change.

The suggested change of paring down to one car per family seems very powerful, but immediately seems to hit a tender spot, too. Giving up one car would have an impact on my independence.

If you are wondering whether you could adjust to life with just one car, try an experiment. Park one of your cars in the garage. Put a tarp over it to help tamper temptation. Then try a month with one car. Keep track of your gas expenses and alternative transportation costs so you can see how your one-car expenses compare to your two-car expenses. Keep notes on compromises you have to make and how you resolved them.

I have already seen from my own figures that combining car trips and cutting back on some car trips altogether makes for substantial savings. See The Fat Dollar’s article on Saving Money on Gas to see how I was able to increase my car’s gas mileage (almost 26%!) by changing my driving habits. Still, the savings from increasing gas mileage is far less than the savings from eliminating a car altogether.

This article from Mother Earth News really resonates with me. I like the article because all of the focus is on increasing quality of life while at the same time needing and spending fewer dollars.

Now that’s The Fat Dollar way!

Patti

While looking through our local grocery store ad, I wondered which cuts of beef (that were on sale) could be used for a recipe I was going to use.

While looking through our local grocery store ad, I wondered which cuts of beef (that were on sale) could be used for a recipe I was going to use.

So how can knowing the right cut of beef save money? Let’s assume that I would like to use my slow cooker to make a beef roast with carrots and potatoes (good assumption!). This week, my local store has Boneless Bottom Round Roast on sale for $3.29 a pound. Knowing that it is perfect as a pot roast (a method of cooking the meat slowly in a covered dish with a small amount of water, broth, or other liquid) allows me to take advantage of this sale price and successfully make a great meal (or meals!)

Generally, my store sells these roasts in 2-3 lb packages. If I plan on about 1 lb per meal for the two of us, then this roast will make one dinner,plus a second dinner of leftovers, and one or more lunches for my husband.

We grow our own potatoes and onions, so I would only need to buy carrots to finish out my slow cooker roast. I pay about $1.00 a pound for organic carrots (about .89 a pound for non-organic) at our Martin’s grocery store.

So with this sale, I could make at least two delicious, low-effort meals for about $4.50 a meal. (Just an estimate since I won’t use a whole pound of carrots, but I might add a couple of biscuits or maybe some fruit, or a small salad, or a bit of dessert.)

However, on the same note, I might have had a bit of culinary disaster if I had purchased this bottom round roast for roasting in the oven for an hour or so. It would likely have turned out tough and dry. Not what I intended, especially if I was cooking it for company!

Oddly, on the flip side, if I had splurged on a tender Top Sirloin Steak ($7.98 a pound this week) and cooked it in the slow cooker, I could easily have ended up with a dry, chewy meal. The Top Sirloin is best cooked by grilling or broiling. It’s low fat content means it will probably be quite dry when slow cooked, even when cooked in liquid. What a waste of an expensive cut of beef! I would have spent over twice as much and gotten a much less delicious meal.

As you can see, you can save money on beef cuts when you know which cut to buy for which recipe or method of cooking.

There are many great reference sites for cuts of beef steaks (round, sirloin, chuck, New York Strip, T-bone, etc). This site has charts that give a description, a photo, the natural tenderness of the cut, and best of all, the alternate names that the cut is sometimes called.

The charts answer my questions and shows which beef cuts are best marinaded first, which can be pan-fried, grilled, broiled, and which ones become tough when overcooked, and which ones are best braised or broiled.

For example, a boneless chuck shoulder steak, normally a bit tough, can make a tender and flavorful meal if it is marinated overnight and not overcooked.

As another example, if you are going to make hamburgers, you will get a much better result with the less expensive 80% lean ground beef. The extra-lean ground beef will not only cost more, but it will cook up dry and chewy.

We don’t eat red meat too often, so having a guide to help me pick out the right beef cuts is perfect. Now when I see a type of beef meat on sale, I can decide whether it will really be a good bargain and how to cook it to make a delicious meal for my family.

How about you? What is your favorite cut of beef for an economical and flavorful meal?

Here are the links to some of the references and charts: http://www.recipetips.com/kitchen-tips/t–357/selecting-beef-cuts.asp

https://www.recipetips.com/kitchen-tips/t–340/beef-steaks.asp

The above sites are from recipetips.com. Here is another example of a good reference.

https://www.beefitswhatsfordinner.com/cuts/collection/33342/best-beef-cuts-for-slow-cooking

Also try Allrecipes.com and TheKitchn.com – there are many good sites with information on cuts of beef.

Here’s to good cooking at great prices! That’s The Fat Dollar way.

Photo courtesy of Fabio Bueno at pexels.com.

Article has been updated from the original.

I unexpectedly found a website from the US Department of Energy that has a feature that tells you the expected mpg (miles per gallon) rating of your car. This includes new and used vehicles. The figures for the used vehicles have been updated to show what mileage the vehicle should currently be getting, as well as what the vehicle was rated for when new.

I unexpectedly found a website from the US Department of Energy that has a feature that tells you the expected mpg (miles per gallon) rating of your car. This includes new and used vehicles. The figures for the used vehicles have been updated to show what mileage the vehicle should currently be getting, as well as what the vehicle was rated for when new.

For example, a 2004 Lexus ES 330 was originally estimated to get a combined highway/city mpg rating of 24. Currently the site estimates the 2019 mileage would be expected to be 21 mpg. Additionally, the site allows input from readers. The actual input from 2004 Lexus ES 330 owners averages 22.5 mpg.

Cool. This is a good tool for determining if your engine needs a tune-up or perhaps your driving habits need some adjusting. If your actual gas mileage for your car falls short of the estimates, you might even want to check your tires. Improperly inflated or over-worn tires can reduce gas mileage, too.

If you are thinking of buying another car, then the site allows you to compare up to four vehicles side by side. You can use this feature to decide which vehicle will have the lowest expected yearly operating costs.

Another good way to use this information is in polishing your monthly expense budget. If you are not sure how much to put on your budget for monthly gasoline expenses, then the site has an estimated gasoline cost per driving mile to help you get started with a figure.

If your driving habits might be the culprit, then visit The Fat Dollar’s article Save Money on Gas where I share the no-cost changes I made to increase my gas mileage by 26%.

Do you know the gas mileage for your car? How does it compare to the official mileage estimates?

Editors Note: Updated 10-17-19

This is the time of year for garage sales … there seems to be one or two in full display nearly every time I run an errand.

This is the time of year for garage sales … there seems to be one or two in full display nearly every time I run an errand.

You might call them tag sales, yard sales, or even moving sales.

If you have been considering a purchase of a small kitchen appliance or specialty gadget, garage sales are a great way to have an inexpensive “trial run” to get an idea of what features are important to you, as well as whether you will even use the item at all. A large majority of small kitchen appliances are rarely used and many of them find their way to garage sales.

For example, bread making machines are a common item to find at garage sales in my area. The average price for a new-looking machine is about $5.00. Yup. $5.00 for a machine that probably cost $60.00 to $100.00 new.

Personally, I love my bread machine. I use it often. But if you visit garage sales in my area, it would seem that I am in the minority, and that many bread machines get used once or twice and then abandoned.

So, in this example, if you have been thinking about buying a bread machine, you could find one at a garage sale and take it home and experiment with it to see if you will actually use it enough to warrant owning one. If so, then using the machine will also help you to decide what features are important to you and if you are satisfied enough to keep the one you bought or if you will now buy a new model with greater confidence of which one to select. If you choose to buy a new machine with better features, the garage sale machine can be given away to a friend or charity for a win-win solution.

My guess is that you’ll save a considerable amount of money on small kitchen appliances this way, especially the specialty ones. Many (if not most!) specialty appliances are used once or twice and then forgotten, given away or sold. Bread makers, waffle makers, ice cream makers, single milk shake mixers, tabletop grills, frozen ice drink makers, pocket sandwich makers, food dehydrators, etc., are the type of appliance that you tend to either really love and use or you find that it’s just too much trouble to get it out, use it, and clean it. Weed out the latter ones with a $5.00 or $10.00 purchase price, rather than spending $75.00 or $100.00 for something that will sit unused in your cabinet.

One important note – whenever you buy a small appliance at a garage sale, take the time to ask the owner if the appliance works and what they did/didn’t like about it. I almost always get an honest answer. Quite often the item is still in the original box and looks barely used. You may even be able to plug the appliance in and see if it works.

My son has been asking for waffles, so I’m on the lookout for a waffle maker. I’ve checked out prices for new ones, so I’ll recognize a true bargain when I see it. Now that he’s been asking, I’m looking forward to having a breakfast of waffles, too! Since I have my doubts that I’ll use a waffle maker often enough to warrant spending a lot of money on one, I’m looking for one in great condition that I can experiment with.

[Update: I found a good waffle maker at our Humane Society’s Red Barn Resale Shop. $2.00! It makes yummy waffles. ]

How about you? Have you found a favorite kitchen appliance at a garage sale? I’d love to hear about your experience.

Have fun looking for and experimenting with your bargain garage sale finds. That’s the Fat Dollar way.

Editor’s Note: this is an updated post from 02-04-12

I’m always delighted when I do something to make my life easier and then find that it saves money, too. In this case, I’m referring to freezing milk for later use.

I’m always delighted when I do something to make my life easier and then find that it saves money, too. In this case, I’m referring to freezing milk for later use.

Milk can be easily frozen. A quart sized canning jar is perfect for freezing milk. Be sure to leave room in the container for the milk to expand as it freezes.

When milk freezes, over time the fats in the milk separate from the water in the milk. To avoid this, freeze milk for very short periods, such as 2 -3 days. Alternatively, you can vigorously shake, stir, or blend the milk after it is thawed to redistribute the fats.

The best way to thaw frozen milk is to put it in the refrigerator overnight. Larger quantities of frozen milk may require longer than a night to thaw. An alternative is to put the sealed frozen milk container in a sink or bowl of cold water to thaw.

At my local grocery stores, milk is currently on sale for $2.50 a gallon. That translates to $.156 per cup. Freezing a quart of fresh milk to prevent it from spoilage and resulting waste will save $.62 (4 cups @ .156/cup) Freezing and later using a quart of milk each week would save $32.24 a year, or the equivalent of over 12 gallons of milk a year.

Even better than the money savings is the convenience of always having milk for cooking and eating. No more special trips to the store for a gallon of milk! That is a big time saver. And hey, that saves gasoline as well. Now that’s The Fat Dollar way.

Related article on The Fat Dollar website (more detailed) – Freezing Milk

Editor’s Note: Article originally published Jun 26 2012

We make a pot of coffee everyday which means that we have a filter full of used coffee grounds everyday. Since we have a septic tank and we don’t want the grounds to build up a sludge inside the tank, we don’t rinse these down the drain. That leaves me curious and looking for uses other than simply tossing them in the garbage can. Over the years, I’ve found a long list of really excellent uses for these grounds.

We make a pot of coffee everyday which means that we have a filter full of used coffee grounds everyday. Since we have a septic tank and we don’t want the grounds to build up a sludge inside the tank, we don’t rinse these down the drain. That leaves me curious and looking for uses other than simply tossing them in the garbage can. Over the years, I’ve found a long list of really excellent uses for these grounds.

Occasionally we will make a second pot of coffee. Since the grounds are already in the filter, I put about 1/2 the usual amount of new grounds right on top of the freshly used ones. It still makes a very good cup of coffee, although not as excellent as that first, smooth, deeply flavored first cup of the morning. Could just be that I’m not as groggy and my taste buds are fully awake by the time we start on the second pot of coffee, though.

It’s nice that the second pot of coffee costs half the price of the first pot. That is a savings of $.50 to $.75, depending on how strong we want the coffee. * If we did this everyday, and still enjoyed the second pot of coffee, the savings would add up nicely.

Beyond that, we have many other excellent uses for the grounds. The one I use most often is to sprinkle them around the rhododendron bush and the blueberry bushes as a mild acid-enriched fertilizer and as a general nitrogen-enhancing additive for the rest of the garden.

Probably the next best use is as an exfolliator and cellulite reducing beauty treatment. Messy, messy, messy, but possibly very nice results. Do an allergy test first if you are going to try this.

I’ve posted an article on The Fat Dollar site, 26 Uses for Used Coffee Grounds … -including using them for repairing scratches in wood, as a scrubbing agent when cleaning, making a treasure stone for the kids, a pesticide, natural deodorizer, a hair rinse … and more!

It feels great to keep something out of your septic tank or landfills and at the same time make a money-saving, very effective use for it. That’s exactly what you can do when you have a second use for your used coffee grounds and that’s The Fat Dollar way!

Don’t forget to have fun finding new uses for the grounds. If you have another use for them, share it with us in the comments below. Thanks!

Patti

Article references: Uses for Used Coffee Grounds – The Fat Dollar

Brewing Best Practices – SCAA of America

* Pricing – Copper Moon World Coffee Hawaiian Hazelnut from Sam’s Club – 2.5 lb for $14.98 – we use 1.75 to 3.0 oz per pot of coffee. Not including the water, electricity or wear on the coffee maker, a pot of coffee will cost between $.78 to $1.41, depending on how strong we want the coffee.

The NCAUSA recommends 1-2 Tablespoons of ground coffee for every 6 ounces of water. This would be 10-21 tablespoons of coffee for each 64 oz pot of coffee. Note that 21 tablespoons would make a very strong cup of coffee! We personally use 10-12 tablespoons of coffee for a 12 cup coffee pot.